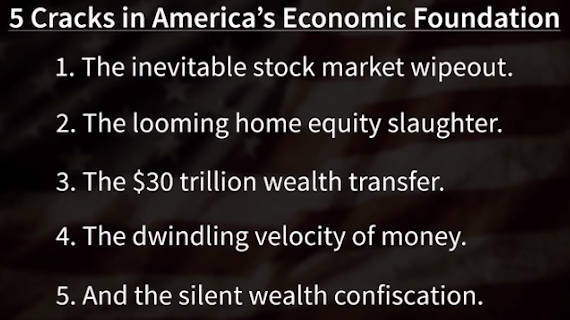

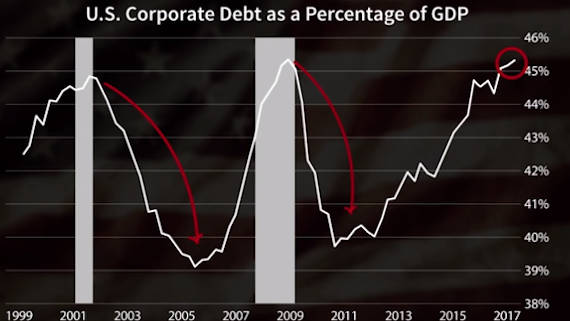

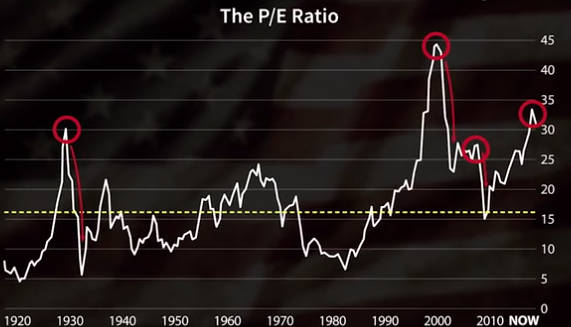

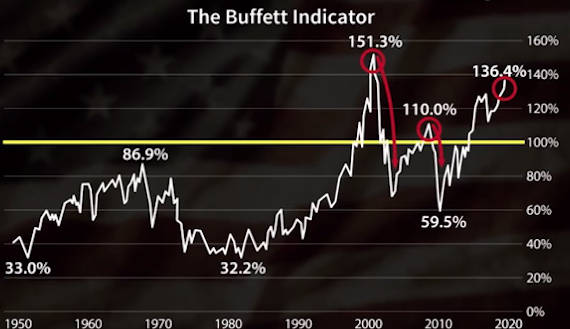

1) Stock Market

Stock Market Indicators

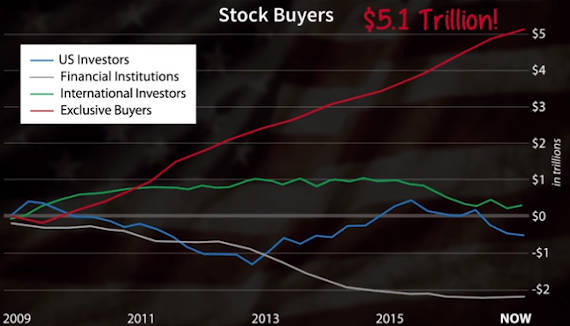

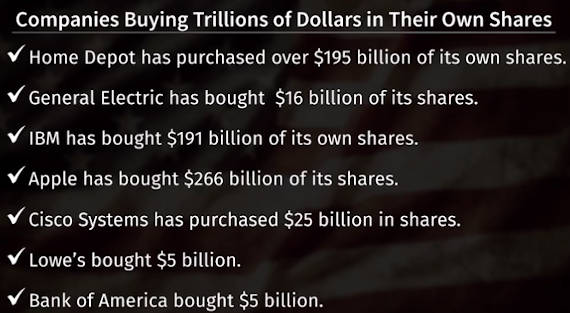

2) Money Extraction

Who is the red line? If you haven't guess it is 'Stock Buy Backs'

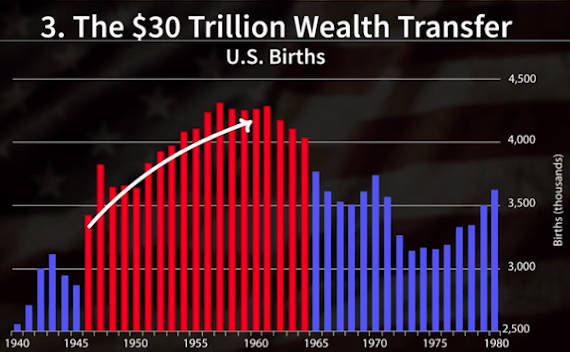

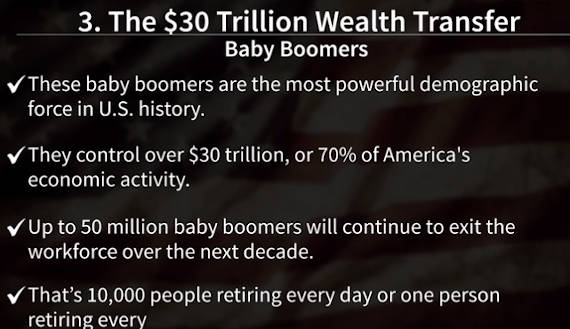

3) Wealth Transfer

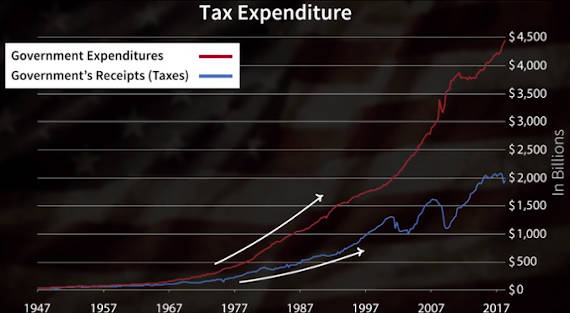

4) Weath Extraction & Wealth Transfers & National Debt (13 images below) Causes:

5) Unemplyment Rate

6) What is Our Credit Card Debt

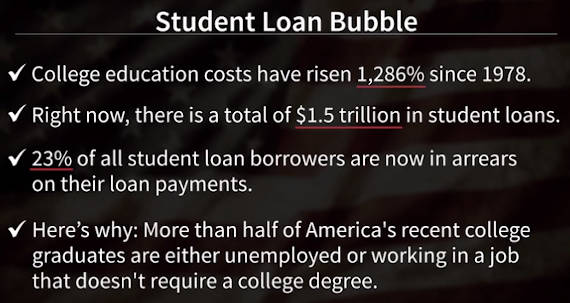

7) What is Our Student Loan Debt

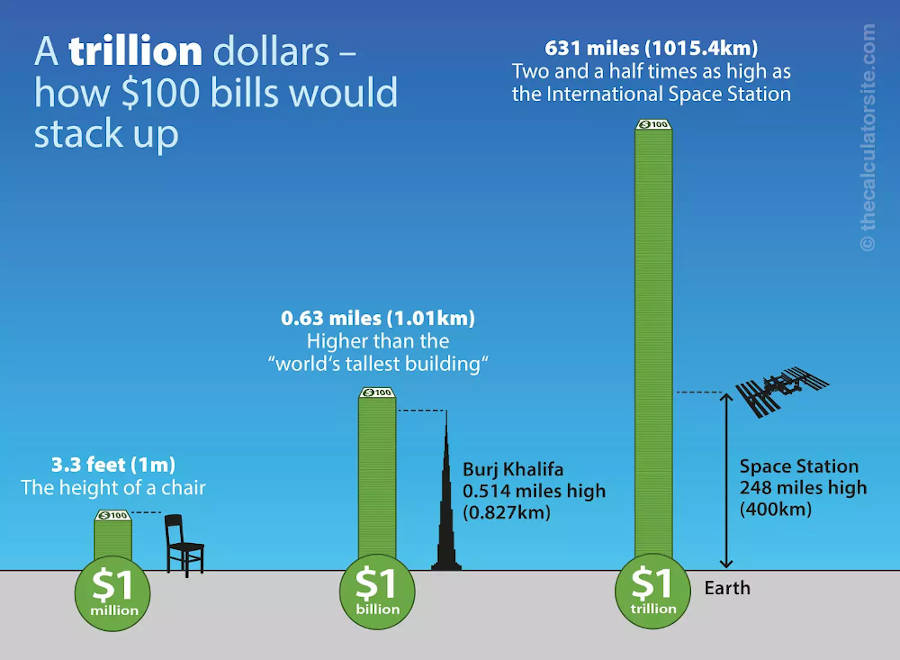

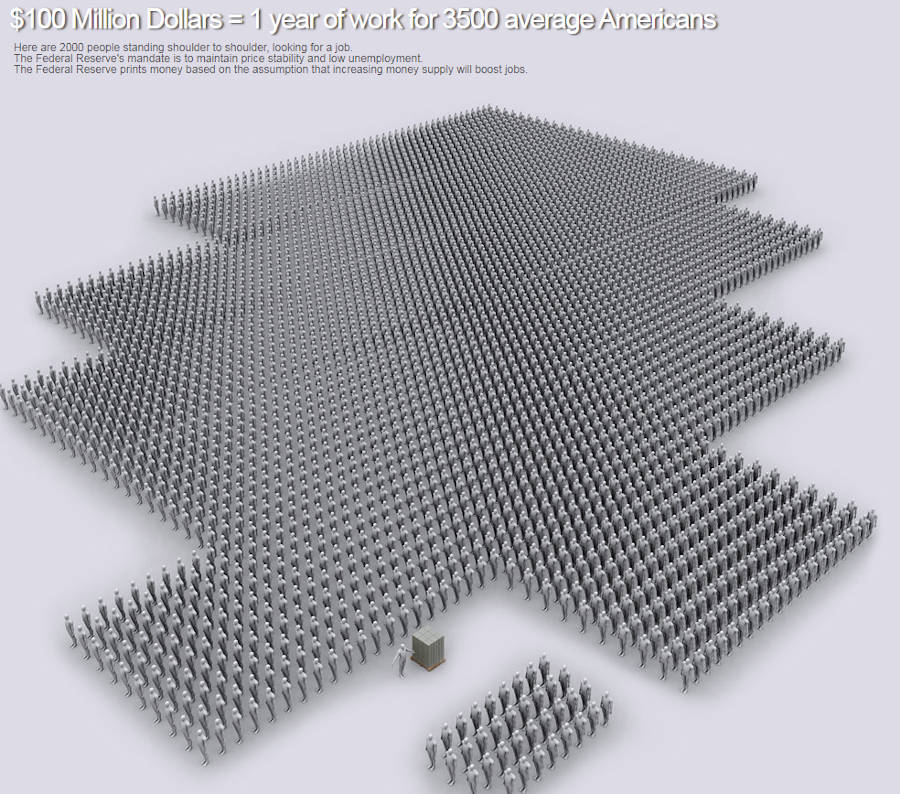

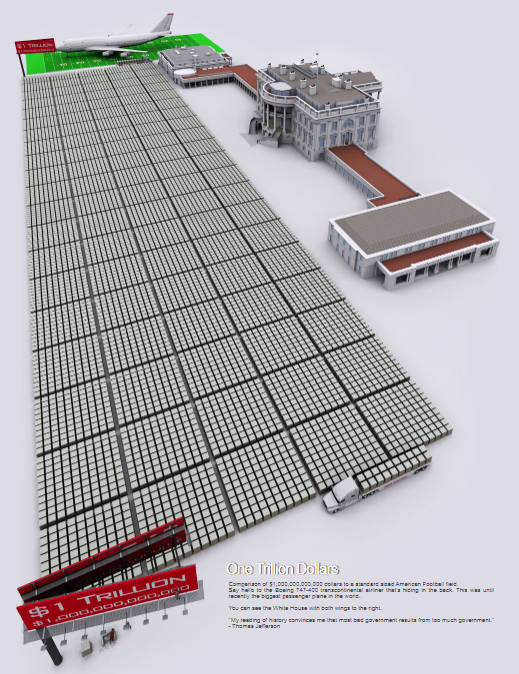

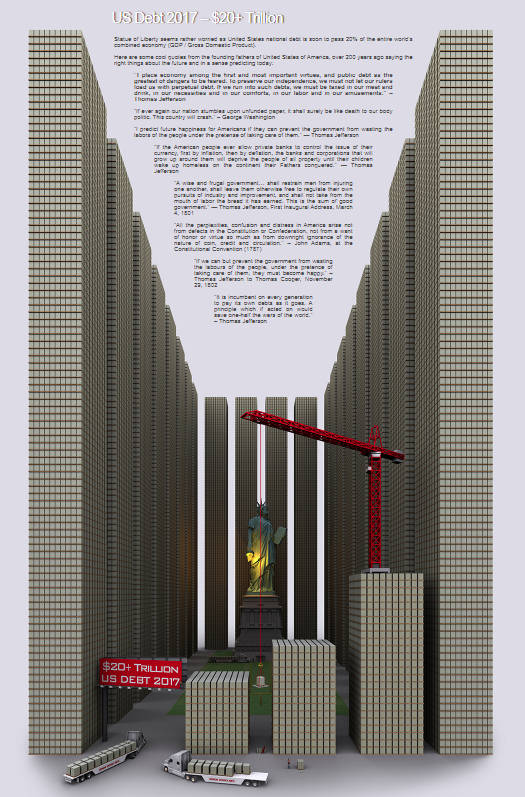

8) What Does a Trillion Dollars Look Like

Keep in Mind

1 Dollar

1 Thousand dollars

1 Million dollars = (thousand thousand dollars)

1 Billion dollars = (thousand million dollars)

1 Trillion dollars = (thousand billion dollars)

1 Quadrillion dollars = (thousand trillion dollars)

1 Dollar

1 Thousand dollars

1 Million dollars = (thousand thousand dollars)

1 Billion dollars = (thousand million dollars)

1 Trillion dollars = (thousand billion dollars)

1 Quadrillion dollars = (thousand trillion dollars)

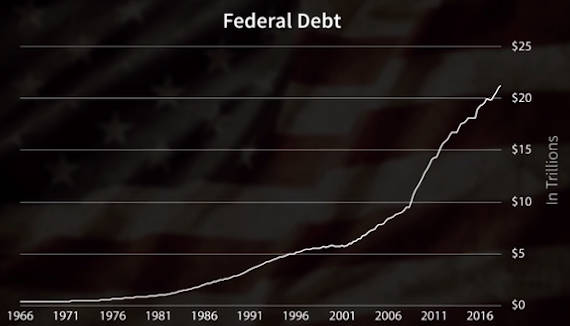

9) What is Our National Debt

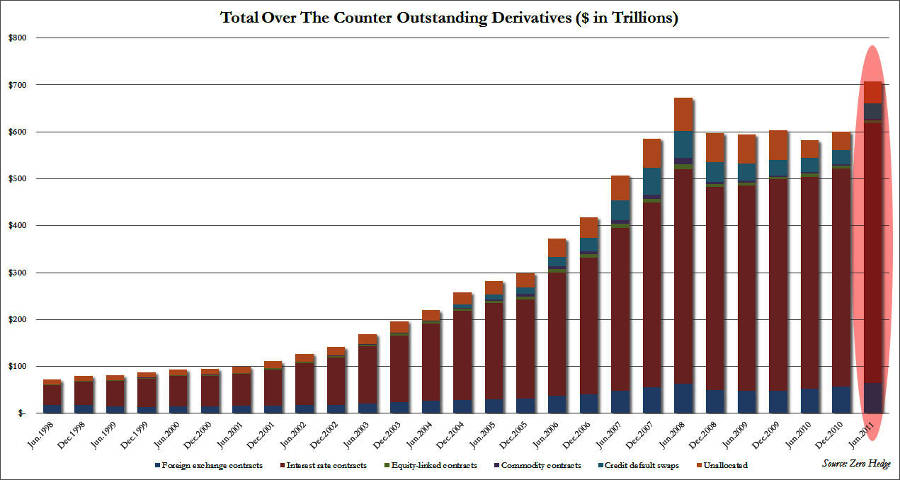

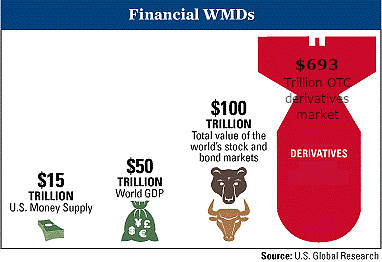

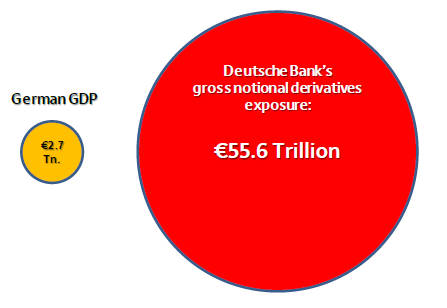

10) Derivatives | Note: this info/graphs/data is sorely out of date and I'm trying to find new data to replace it. But it gives you the jest of the problem.

Note: The following graphs are from 2008, 2010, 2011, it seems like we don't track this stuff anymore!

Who Own the Derivative Time Bomb in the US? (2011)

Five Banks Account For 96% Of The $250 Trillion In Outstanding US Derivative Exposure; Is Morgan Stanley Sitting On An FX Derivative Time Bomb?

The latest quarterly report from the Office Of the Currency Comptroller is out and as usual it presents in a crisp, clear and very much glaring format the fact that the top 4 banks in the US now account for a massively disproportionate amount of the derivative risk in the financial system. Specifically, of the $250 trillion in gross notional amount of derivative contracts outstanding (consisting of Interest Rate, FX, Equity Contracts, Commodity and CDS) among the Top 25 commercial banks (a number that swells to $333 trillion when looking at the Top 25 Bank Holding Companies), a mere 5 banks (and really 4) account for 95.9% of all derivative exposure (HSBC replaced Wells as the Top 5th bank, which at $3.9 trillion in derivative exposure is a distant place from #4 Goldman with $47.7 trillion). The top 4 banks: JPM with $78.1 trillion in exposure, Citi with $56 trillion, Bank of America with $53 trillion and Goldman with $48 trillion, account for 94.4% of total exposure. As historically has been the case, the bulk of consolidated exposure is in Interest Rate swaps ($204.6 trillion), followed by FX ($26.5TR), CDS ($15.2 trillion), and Equity and Commodity with $1.6 and $1.4 trillion, respectively.

Five Banks Account For 96% Of The $250 Trillion In Outstanding US Derivative Exposure; Is Morgan Stanley Sitting On An FX Derivative Time Bomb?

The latest quarterly report from the Office Of the Currency Comptroller is out and as usual it presents in a crisp, clear and very much glaring format the fact that the top 4 banks in the US now account for a massively disproportionate amount of the derivative risk in the financial system. Specifically, of the $250 trillion in gross notional amount of derivative contracts outstanding (consisting of Interest Rate, FX, Equity Contracts, Commodity and CDS) among the Top 25 commercial banks (a number that swells to $333 trillion when looking at the Top 25 Bank Holding Companies), a mere 5 banks (and really 4) account for 95.9% of all derivative exposure (HSBC replaced Wells as the Top 5th bank, which at $3.9 trillion in derivative exposure is a distant place from #4 Goldman with $47.7 trillion). The top 4 banks: JPM with $78.1 trillion in exposure, Citi with $56 trillion, Bank of America with $53 trillion and Goldman with $48 trillion, account for 94.4% of total exposure. As historically has been the case, the bulk of consolidated exposure is in Interest Rate swaps ($204.6 trillion), followed by FX ($26.5TR), CDS ($15.2 trillion), and Equity and Commodity with $1.6 and $1.4 trillion, respectively.

The Worlds Outstanding Derivatives (has been estimated) => 1.2 Quadrillion Dollars (1 quadrillion is thousand trillion)